Caught in the Middle: The Sandwich Generation

There is an old saying about being caught between a rock and a hard place. Many people might feel that way about providing financial support to children and aging parents while also trying to save for retirement and meet daily financial needs. Dubbed the “sandwich generation,” this group may be growing as people live longer and young adults face challenges that make it more difficult to launch into fully independent lives.

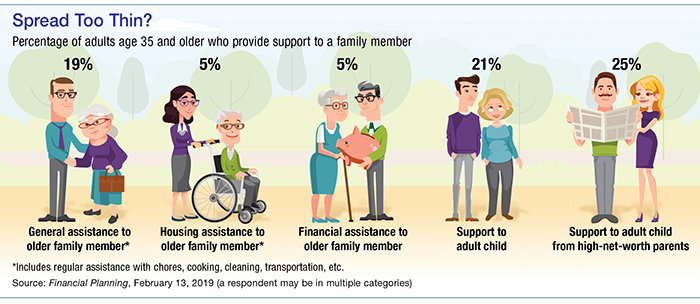

A 2018 survey found that 19% of adults age 35 and older were providing support to an older family member, and 21% were supporting a child over age 18.1 An earlier study of middle-aged adults (ages 40 to 59) found that 15% were providing financial support to an aging parent (65 or older) while also raising a young child or financially supporting an adult child.2

If you find yourself caught in the middle — or if you are an “open-face sandwich” supporting an elderly parent or an adult child — here are some tips to consider.

Communicate and set limits. Older people may be reluctant to discuss their financial situations, but you can’t help unless you understand your parents’ financial resources and obligations. Help set up a budget, including long-term care needs. Don’t volunteer your own funds unless it is absolutely necessary and you can afford it. Depending on the situation, it may be better to spend down an older person’s assets in order to trigger eligibility for Medicaid and other government programs.

Be open with your children about the limitations of your financial resources, and set reasonable goals and guidelines. A college student should bear at least some financial responsibility, working and/or taking student loans, and it is not unreasonable to limit college choices based on affordability. Financial help for an adult child might be given in the form of a loan with a defined repayment plan. A working adult child who lives with you should pay some rent and help with other household responsibilities.

Have an estate plan. Be sure that you, your parents, and any adult children all have current wills and other appropriate documents, such as powers of attorney for health care and finances. A transfer-on-death deed may keep the family home out of probate in some states, while a trust may provide broader asset protection and help control funds. An incentive trust might provide your child with funds only at certain ages or after accomplishing certain milestones. A special-needs trust may help maintain eligibility for government programs for a disabled child or adult. These are just examples; trusts can be constructed to address almost any situation.

Get professional help. When faced with competing and potentially emotional financial priorities, you may benefit from a financial professional who can examine your situation objectively and help you balance the needs of your loved ones with your own financial stability and future goals.

While trusts offer numerous advantages, they incur up-front costs and often have ongoing administrative fees. The use of trusts involves a complex web of tax rules and regulations. You should consider the counsel of an experienced estate planning professional and your legal and tax advisers before implementing such strategies.

Although there is no assurance that working with a financial professional will improve investment results, a professional who focuses on your overall objectives can help you consider strategies that could have a substantial effect on your long-term financial situation.

1) Financial Planning, February 13, 2019

2) Pew Research, 2013 (most recent data available)

This information is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2019 Broadridge Investor Communication Solutions, Inc.

|

LPL Financial Representatives offer access to Trust Services through The Private Trust Company N.A., an affiliate of LPL Financial. |

|

|